An excerpt from The Aspirational Investor: Taming the Markets to Achieve Your Life’s Goals that I think you’d enjoy.

Most of us have a healthy understanding of risk in the short term.

When crossing the street, for example, you would no doubt speed up to avoid an oncoming car that suddenly rounds the corner.

Humans are wired to survive: it’s a basic instinct that takes command almost instantly, enabling our brains to resolve ambiguity quickly so that we can take decisive action in the face of a threat.

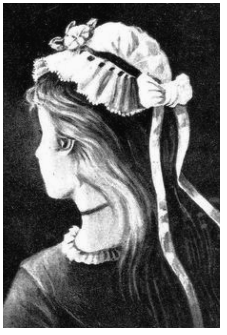

The impulse to resolve ambiguity manifests itself in many ways and in many contexts, even those less fraught with danger. Glance at the (above) picture for no more than a couple of seconds. What do you see?

Some observers perceive the profile of a young woman with flowing hair, an elegant dress, and a bonnet. Others see the image of a woman stooped in old age with a wart on her large nose. Still others—in the gifted minority—are able to see both of the images simultaneously.

What is interesting about this illusion is that our brains instantly decide what image we are looking at, based on our first glance. If your initial glance was toward the vertical profile on the left-hand side, you were all but destined to see the image of the elegant young woman: it was just a matter of your brain interpreting every line in the picture according to the mental image that you already formed, even though each line can be interpreted in two different ways. Conversely, if your first glance fell on the central dark horizontal line that emphasizes the mouth and chin, your brain quickly formed an image of the older woman.

Regardless of your interpretation, your brain wasn’t confused. It simply decided what the picture was and filled in the missing pieces. Your brain resolved ambiguity and extracted order from conflicting information.

What does this have to do with decision making? Every bit of information can be interpreted differently according to our perspective. Ashvin Chhabra directs us to investing. I suggest you reframe this in the context of decision making in general.

Every trade has a seller and a buyer: your state of mind is paramount. If you are in a risk-averse mental framework, then you are likely to interpret a further fall in stocks as additional confirmation of your sell bias. If instead your framework is positive, you will interpret the same event as a buying opportunity.

The challenge of investing is compounded by the fact that our brains, which excel at resolving ambiguity in the face of a threat, are less well equipped to navigate the long term intelligently. Since none of us can predict the future, successful investing requires planning and discipline.

Unfortunately, when reason is in apparent conflict with our instincts—about markets or a “hot stock,” for example—it is our instincts that typically prevail. Our “reptilian brain” wins out over our “rational brain,” as it so often does in other facets of our lives. And as we have seen, investors trade too frequently, and often at the wrong time.

One way our brains resolve conflicting information is to seek out safety in numbers. In the animal kingdom, this is called “moving with the herd,” and it serves a very important purpose: helping to ensure survival. Just as a buffalo will try to stay with the herd in order to minimize its individual vulnerability to predators, we tend to feel safer and more confident investing alongside equally bullish investors in a rising market, and we tend to sell when everyone around us is doing the same. Even the so-called smart money falls prey to a herd mentality: one study, aptly titled “Thy Neighbor’s Portfolio,” found that professional mutual fund managers were more likely to buy or sell a particular stock if other managers in the same city were also buying or selling.

This comfort is costly. The surge in buying activity and the resulting bullish sentiment is self-reinforcing, propelling markets to react even faster. That leads to overvaluation and the inevitable crash when sentiment reverses. As we shall see, such booms and busts are characteristic of all financial markets, regardless of size, location, or even the era in which they exist.

Even though the role of instinct and human emotions in driving speculative bubbles has been well documented in popular books, newspapers, and magazines for hundreds of years, these factors were virtually ignored in conventional financial and economic models until the 1970s.

This is especially surprising given that, in 1951, a young PhD student from the University of Chicago, Harry Markowitz, published two very important papers. The first, entitled “Portfolio Selection,” published in the Journal of Finance, led to the creation of what we call modern portfolio theory, together with the widespread adoption of its important ideas such as asset allocation and diversification. It earned Harry Markowitz a Nobel Prize in Economics.

The second paper, entitled “The Utility of Wealth” and published in the prestigious Journal of Political Economy, was about the propensity of people to hold insurance (safety) and to buy lottery tickets at the same time. It delved deeper into the psychological aspects of investing but was largely forgotten for decades.

The field of behavioral finance really came into its own through the pioneering work of two academic psychologists, Amos Tversky and Daniel Kahneman, who challenged conventional wisdom about how people make decisions involving risk. Their work garnered Kahneman the Nobel Prize in Economics in 2002. Behavioral finance and neuroeconomics are relatively new fields of study that seek to identify and understand human behavior and decision making with regard to choices involving trade-offs between risk and reward. Of particular interest are the human biases that prevent individuals from making fully rational financial decisions in the face of uncertainty.

As behavioral economists have documented, our propensity for herd behavior is just the tip of the iceberg. Kahneman and Tversky, for example, showed that people who were asked to choose between a certain loss and a gamble, in which they could either lose more money or break even, would tend to choose the double down (that is, gamble to avoid the prospect of losses), a behavior the authors called “loss aversion.” Building on this work, Hersh Shefrin and Meir Statman, professors at the University of Santa Clara Leavey School of Business, have linked the propensity for loss aversion to investors’ tendency to hold losing investments too long and to sell winners too soon. They called this bias the disposition effect.

The lengthy list of behaviorally driven market effects often converge in an investor’s tale of woe. Overconfidence causes investors to hold concentrated portfolios and to trade excessively, behaviors that can destroy wealth. The illusion of control causes investors to overestimate the probability of success and underestimate risk because of familiarity—for example, causing investors to hold too much employer stock in their 401(k) plans, resulting in under-diversification. Cognitive dissonance causes us to ignore evidence that is contrary to our opinions, leading to myopic investing behavior. And the representativeness bias leads investors to assess risk and return based on superficial characteristics—for example, by assuming that shares of companies that make products you like are good investments.

Several other key behavioral biases come into play in the realm of investing. Framing can cause investors to make a decision based on how the question is worded and the choices presented. Anchoring often leads investors to unconsciously create a reference point, say for securities prices, and then adjust decisions or expectations with respect to that anchor. This bias might impede your ability to sell a losing stock, for example, in the false hope that you can earn your money back. Similarly, the endowment bias might lead you to overvalue a stock that you own and thus hold on to the position too long. And regret aversion may lead you to avoid taking a tough action for fear that it will turn out badly. This can lead to decision paralysis in the wake of a market crash, even though, statistically, it is a good buying opportunity.

Behavioral finance has generated plenty of debate. Some observers have hailed the field as revolutionary; others bemoan the discipline’s seeming lack of a transcendent, unifying theory. This much is clear: behavioral finance treats biases as mistakes that, in academic parlance, prevent investors from thinking “rationally” and cause them to hold “suboptimal” portfolios.

But is that really true? In investing, as in life, the answer is more complex than it appears. Effective decision making requires us to balance our “reptilian brain,” which governs instinctive thinking, with our “rational brain,” which is responsible for strategic thinking. Instinct must integrate with experience.

Put another way, behavioral biases are nothing more than a series of complex trade-offs between risk and reward. When the stock market is taking off, for example, a failure to rebalance by selling winners is considered a mistake. The same goes for a failure to add to a position in a plummeting market. That’s because conventional finance theory assumes markets to be inherently stable, or “mean-reverting,” so most deviations from the historical rate of return are viewed as fluctuations that will revert to the mean, or self-correct, over time.

But what if a precipitous market drop is slicing into your peace of mind, affecting your sleep, your relationships, and your professional life? What if that assumption about markets reverting to the mean doesn’t hold true and you cannot afford to hold on for an extended period of time? In both cases, it might just be “rational” to sell and accept your losses precisely when investment theory says you should be buying. A concentrated bet might also make sense, if you possess the skill or knowledge to exploit an opportunity that others might not see, even if it flies in the face of conventional diversification principles.

Of course, the time to create decision rules for extreme market scenarios and concentrated bets is when you are building your investment strategy, not in the middle of a market crisis or at the moment a high-risk, high-reward opportunity from a former business partner lands on your desk and gives you an adrenaline jolt. A disciplined process for managing risk in relation to a clear set of goals will enable you to use the insights offered by behavioral finance to your advantage, rather than fall prey to the common pitfalls. This is one of the central insights of the Wealth Allocation Framework. But before we can put these insights to practical use, we need to understand the true nature of financial markets.